How to use the DRYIT semi-continuous tray dryer

Practical Action

The basic aim of any industrial processing operation is to make sure that the value being

added per ton of production is greater than the total of all the costs involved in producing and

selling it.

In the case of drying the main production cost areas needing consideration are:

• Raw material cost per unit of usable raw material

• The product drying ratio i.e. kg of dry product from 100 kg fresh material

• Fuel costs

• Labour

• Packaging

• Equipment costs and depreciation

• Distribution, marketing etc

• Rent

• Overheads

While a full analysis of all the above is essential to develop a business plan this section will

concentrate on the first four areas as they involve crop processing and technical selections

that conventional business advisors may not be able to provide.

Raw material cost per unit of usable raw material

No incoming raw material will be totally usable; there is always some wastage through second

grade and damaged material and preparation (skinning, stoning, selecting etc) prior to drying.

It is recommended that a quantity of raw material is purchased, weighed and then prepared

for the dryer.

Wt. Fresh material x cost/kg = cost /kg prepared material

Wt. prepared material

This preparation ration can vary through two main factors. Firstly, the nature and variety of

the raw material and, secondly, the quality delivered by the supplier. It may therefore be

useful to examine both these aspects.

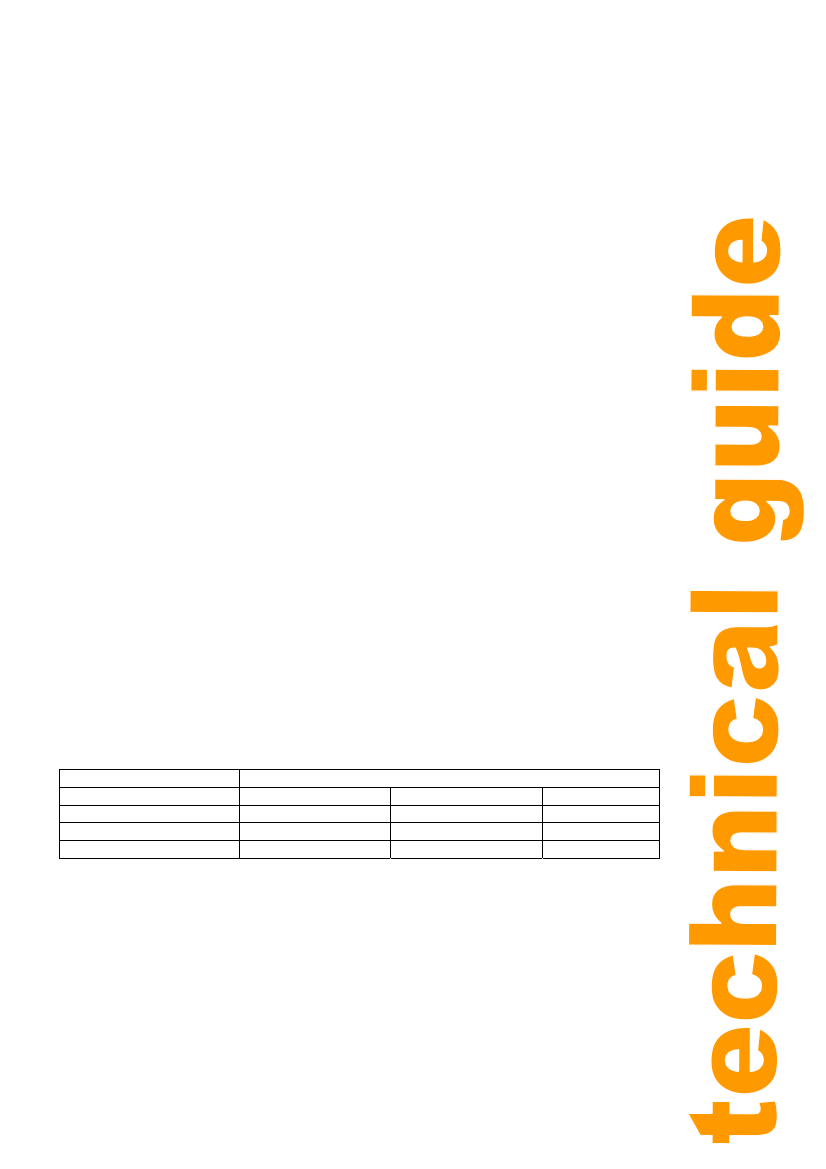

For example, in the production of dry mango a quantity of 3 varieties were purchased from 3

different suppliers and the following test was carried out.

Supplier A

Supplier B

Supplier C

% of damaged, low grade fruit rejected

Variety 1

Variety 2

10 8

86

13 11

Variety 3

14

10

20

This indicates that supplier B is likely to be more reliable and also that variety 3 is more

susceptible to damage.

7